In the spring of 2026, I spoke at CoBank’s annual series of regional customer meetings about the work of a new commission focused on driving growth and economic resiliency in America’s rural communities. The bipartisan commission was formed in the 2025 by two prominent think tanks in Washington, D.C. — the Brookings Institution and the American Enterprise Institute. The official name of the commission is The Brookings-AEI Commission on U.S. Rural Prosperity.

The work of the commission is still in its early stages. We are in the process of holding “field hearings” in various rural areas across the country — meeting with local business and political leaders and learning about the challenges and opportunities their communities face. The goal is to produce a comprehensive public report, including thoughtful rural policy recommendations, in advance of the Congressional and presidential federal election cycle in 2028.

This picture was taken last fall at Grand Farm in Casselton, North Dakota, about half an hour west of Fargo. Grand Farm is a nonprofit research organization focused on promoting American agriculture — how we can ensure the U.S. farm economy is positioned for long-term success using technological innovation. I’m in the middle, wearing the black hat, watching a technology demonstration by the Grand Farm staff.

For the benefit of those who weren’t at our customer meetings, I'm sharing five key themes that I am personally focused on as a member of the commission — and as the CEO of a financial institution that lends exclusively to rural industries.

I am also asking for feedback on the questions the commission is exploring, and what policy changes will drive the most positive impact across rural America. If you have ideas you are willing to share, please do so using the link at the end of this report. I will read every comment that is submitted, and make sure it gets shared with the commission staff as they prepare their final report.

Understanding the dimensions of the U.S. rural economy

Rural America is a big, multifaceted and highly complex geographic space — actually, a broad spectrum of places.

By most estimates, it makes up something like 97% of the land mass of the United States, even though it is home to only about 20% of the U.S. population.

It encompasses over 3 million square miles of territory — regions and areas with vastly different climates, economies, landscapes, histories and demographic profiles.

That makes it a challenging task to even define the rural economy’s key attributes, let alone come up with policy prescriptions that will drive economic development and prosperity across its entire diversity.

Last year, McKinsey, the global business consulting firm, published an excellent report in which they set out to comprehensively define the rural economy of the United States. It is available publicly.

What McKinsey did was create a giant database of every rural county in the United States — almost 2,000 counties in total.

Under this taxonomy, every rural county is classified into one of six different categories, which McKinsey calls “archetypes”.

Not surprisingly, one major category of rural areas is those where production agriculture is a major contributor of economic output. In McKinsey’s methodology, they used a threshold of 20% or more of local GDP.

These agriculture-dependent counties make up about a fifth of all the rural counties in America by number. However, these counties account for only 7% of the total rural population in the United States — and only about 8% of rural GDP.

Another major category is counties where extraction industries like mining or oil and gas exploration are dominant. Only 9% of counties fell into this category, representing 5% of the rural population and 11% of rural GDP.

Yet another archetype is counties where manufacturing is a major source of business investment and employment. These counties comprise about 25% of the rural population and almost 30% of rural GDP.

Another is the group of rural counties that are either in the exurbs of large cities or that benefit from a lot of tourism.

There is also a set of rural counties that are struggling economically and under-performing relative to their peers, with declining population and below-average GDP performance.

Finally, there is a catch-all group called “Middle America” — counties that are rural but where the local economy is diverse enough that they don’t fall neatly into any of the other categories.

There's room for discussion about whether McKinsey's framework leaves out important components of the rural economy, but at the end of the day, I think we do need a simple and straightforward framework like this for policymakers to use.

Key issue no. 2

Headwinds for agriculture

Production agriculture today accounts for less than 10% of rural GDP output in the United States — and less than 1% of our national GDP.

And yet it dominates the rural landscape — something like 40% of the country’s physical space is allocated to crop production or pastureland.

More importantly, agriculture is essential for our national security, enabling America to feed itself in a self-sufficient manner while also supplying high-quality food products to people all over the world.

But key sectors of the U.S. farm economy — row crops in particular — are struggling due to a variety of factors including low prices for ag commodities, elevated input costs, and the impacts of tariffs and trade wars.

The key question from my standpoint is as follows:

Is the current downturn in row crop production agriculture cyclical, meaning it could turn around relatively quickly through normal market mechanisms of price and output adjustments?

Or is the current downturn in row crop production ag structural, meaning it will be more prolonged, more severe, and more challenging to resolve given long-term trends in the global marketplace?

There is a lot of evidence out there that it is structural.

According to USDA’s most recent estimates for the 2026 fiscal year, exports by volume this year will be at about 160 million metric tons, which is higher than in 2022 when exports boomed in the wake of Russia’s invasion of Ukraine.

By value, based on USDA’s projections, exports will be down more than 30% in 2026 from where they were five years ago.

It’s disconcerting to see our nation’s farmers exporting near-record levels of crops on a volume basis but getting so much less cash for those sales in return.

On top of those marketplace headwinds, there are arguably fewer policy levers for policymakers to help agriculture than they had at their disposal in an earlier era.

That’s illustrated by this chart, which shows U.S. corn and soybean production going back to 1990.

Several key events have helped American farmers find a home for our ever-increasing production:

The “freedom to farm” provision in the 1996 Farm Bill;

China joining the WTO in 2001;

And the expansion of the Renewable Fuel Standard for corn-based ethanol in 2007.

To use an agricultural metaphor, we have picked most of the low-hanging fruit from a policy perspective.

This is another reason why the downturn feels structural rather than cyclical.

It goes without saying that we must find a path forward here that protects America’s farm economy and creates viable markets for our output in the future.

Consistent federal policy, including a consistently updated Farm Bill, would be a great place to start.

If we can just do that — provide a set of rules for producers that are stable and predictable — I am confident that farmers will figure out a way to be successful and remain the most efficient and productive in the world.

Key issue no. 3

Electricity supply and demand

What are we going to do about the emerging supply-demand imbalance in the U.S. electric power complex? That imbalance is being driven by investment in artificial intelligence and the dynamically growing energy requirements of AI data centers.

Rural America is right in the middle of this trend. About two thirds of data centers currently in planning stages in the United States will be in rural areas, according to a recent report from Pew Research Center.

AI is driving a ton of interest and investment in rural communities, and we are early in the development of this trend.

Rural communities will have important choices to make about these facilities — including the hundreds of electric cooperatives that CoBank finances all over the country.

For a period of about two decades, demand for electricity in the United States was essentially flat.

The amount of electricity our economy consumed in 2024 wasn’t much higher than it was way back in 2010 — even though both our population and the size of the U.S. economy increased substantially.

This low growth in demand was due to a couple key factors — homes and commercial buildings becoming more energy-efficient — and the increased share of services in the economy vs. energy-intensive sectors like manufacturing.

All that is changing — and changing rapidly.

The forecast for U.S. electricity consumption now looks far different. Estimates vary widely, but there is strong consensus that it will grow thanks to AI, electric vehicles and other new sources of demand.

That’s a very significant change compared to what the industry has been accustomed to for the last several decades.

Whether our national power grid is up to the task to meet this surging demand is a big question.

That’s illustrated by this map, which was released in January 2026 as part of a long-term reliability assessment put out by industry every year.

The colored sections of the map indicate where electric generation capacity is projected to fall below industry standard reserve margins over the next 10 years.

As you can see, it is most of the United States, and Canada as well.

According to this forecast, the dark red areas in the middle of the country will start to see capacity shortfalls as early as 2028.

Other regions have a longer runway but are still at risk through 2035.

Like the situation with agriculture, this is another critical issue that our country really has to get right.

Key issue no. 4

Demographic trends impacting rural America

Since the COVID pandemic in 2020, we’ve seen a significant shift in migration patterns across the U.S. due to the rise of remote work and other trends.

Many people have left big cities for other parts of the country seeking a lower cost of living and a better quality of life. And I think that's an important macro trend impacting the economic outlook for rural areas.

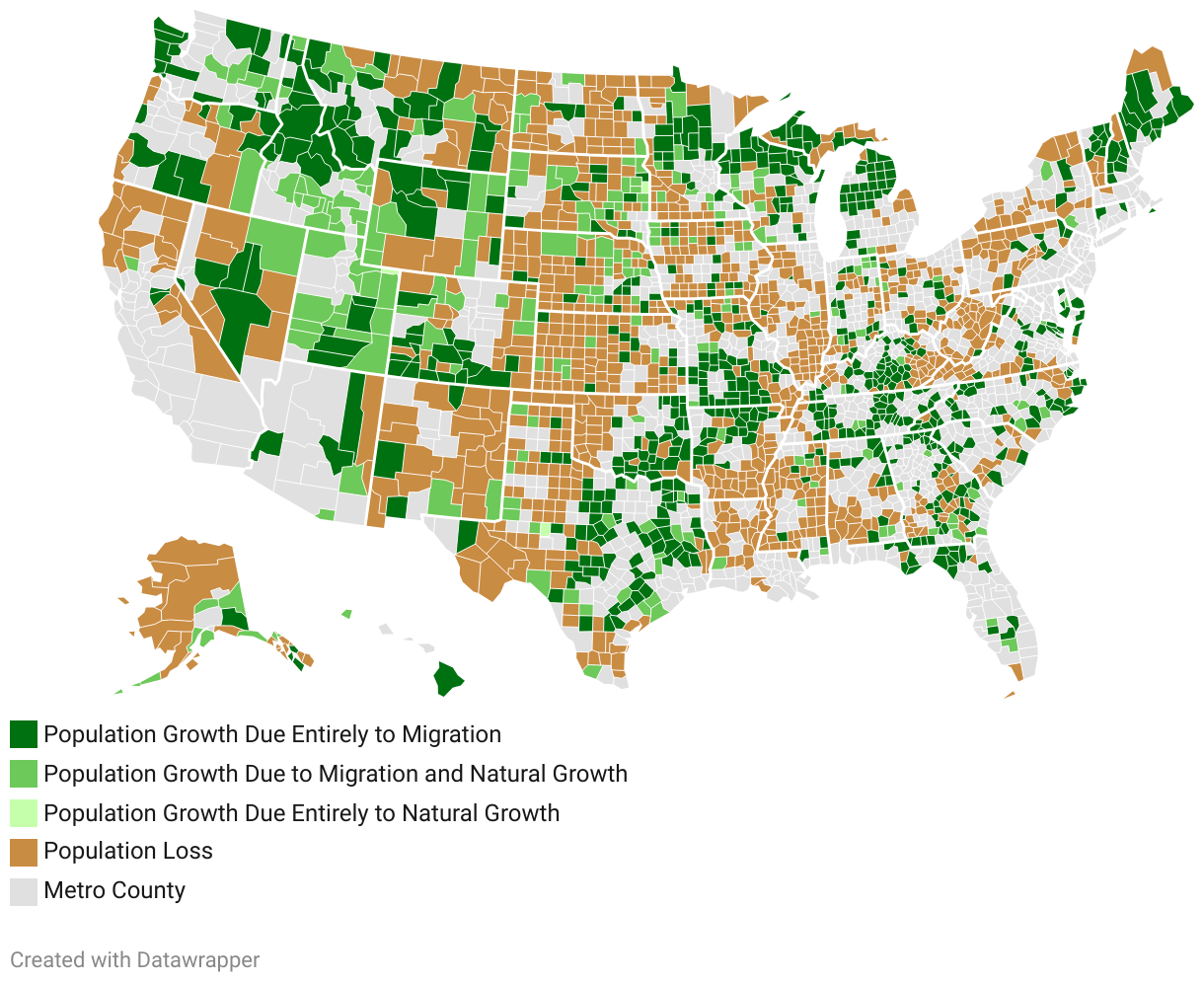

Harvard University recently published a report on this, contrasting the change in rural population growth trends before and after the pandemic.

In the four-year period leading up to 2020, the country’s rural population actually declined a little bit, by about 60,000 people. More Americans were leaving rural places than were moving in. And the rate of natural change was also negative, meaning there were fewer births than deaths.

Things have really turned around over the last couple of years. The rural population grew by over 430,000 people from 2021 to 2024. A substantial portion of that growth was due to urban outmigration.

It’s important to keep in mind that the benefits of this trend are not evenly distributed. Harvard put together a map color-coding all the rural counties in the United States. Green areas have grown in the post-pandemic period; brown areas have lost population.

This trend certainly bears watching and will continue to shape the demographic profile of rural America in the years ahead.

Key issue no. 5

Rural-urban interdependence

Another major issue facing rural America is the growing political divide separating urban and rural places.

A Pew Research Center report showed that people in America’s suburbs, interestingly enough, are split pretty evenly between Republicans and Democrats.

But look at how big the divide has become between urban and rural voters on the left and right.

The Democratic Party absolutely dominates in cities.

The Republican Party is just as dominant in rural areas.

The key thing to worry about here is not that we have political divisions — that will always be the case in a country as large and diverse as the United States.

It’s that the division has become so decidedly place-based.

That is never a healthy dynamic in a democratic republic like ours. During the Civil War it was the North against the South. Today I worry we are becoming urban versus rural.

And it is something we need to fix, because the fact is that urban American and rural America depend on each other in countless ways.

Rural America supplies urban America with virtually all of its food, fiber and energy.

Meanwhile, urban America provides rural America with markets — and a lot of financial support as well.

In rural counties, federal transfer payments — which include programs like Medicare, Medicaid and Social Security — account for 25% of total personal income — much higher than the national average.

That’s because, on average, rural areas have higher poverty rates and a higher average age of the population.

I believe it is in no one’s long term best interest to see political polarization get worse in our country than it is today.

I hope that all of our customers, as leaders of rural businesses, will help to be part of the solution and not part of the problem.

We want to hear from you

CoBank and its customers can be a valuable source of information and experience for the Brookings-AEI commission staff and members. So can all my followers on LinkedIn who work in rural industries. They are at the proverbial coalface of rural economic output in this country — running businesses that form the foundation of the rural economy.

You can submit your unique ideas and suggestions to the commission for how to drive future prosperity in rural America. Fill out the form and I will collect and collate every comment we receive and provide it to the commission for inclusion in its deliberations and ultimate report.

Thanks to all who submit their comments and perspectives!

{kind=link}